Introduction

Procurement transformation has emerged as a critical initiative for organizations seeking to stay competitive and adapt to changing market dynamics. At its core, digital procurement transformation involves reimagining and optimizing procurement processes, technologies and strategies to drive greater procurement efficiency, cost savings, and value across the supply chain.

Hackett’s CPO Key Issues Study revealed that 89% of respondents agree or strongly agree that their talent and business needs will fundamentally change by digital technologies. Additionally, the vast majority (84%) think digital transformation will improve procurement performance and service delivery over the next 3-5 years.

Businesses that want to optimize their procurement operations and gain a competitive edge will need to start digitally transforming their procurement processes. However, procurement transformation is not without its challenges, such as resistance to change, lack of skills, and data issues.

In this article, we’ll examine the concept of procurement transformation, the steps for creating a successful procurement transformation strategy and how to create value along the S2P & P2P processes. We’ll also illustrate the benefits of procurement automation and explain how IKEA leverages Ivalua’s procurement platform to cut costs and improve efficiencies throughout the procure-to-pay process.

Key Takeaways

- Procurement transformation is a strategic necessity for organizations aiming to stay competitive and resilient.

- AI and automation are key to improving procurement efficiency, decision-making, and supplier collaboration.

- A phased approach with the right technology partner enables quick wins and long-term scalability.

What Is Procurement Transformation?

Procurement Transformation refers to the comprehensive overhaul and enhancement of procurement processes, strategies, technologies and organizational structures to drive significant improvements in efficiency, effectiveness and value creation within the procurement process.

It requires a reimagining of traditional procurement practices and the implementation of innovative approaches to optimize sourcing, supplier management, contract negotiation, purchasing and other procurement activities.

Procurement transformation takes purchasing tasks and elevates them, making them an integral element embedded into your standard business processes, set to affect current and future success. It provides a reliable framework that focuses on shifting your Procurement department from a tactical cost center to a strategic value-added function.

The end goal is to align strategic procurement practices with organizational objectives, enhance collaboration with suppliers, mitigate risks, improve compliance and drive cost savings and value generation across the supply chain.

While, 86% of respondents to a Digital Readiness Assessment of Procurement Leaders said that they lacked at least one foundational capability for digital transformation, procurement leadership teams recognize the potential benefits of digital transformation. And, while many organizations have faced challenges in harnessing these opportunities, using the right procurement software, roadmap and processes can help them be successful.

What Are The Benefits of Procurement Transformation?

By integrating a procurement automation solution, companies of all sizes can expect a substantial boost in operational efficiency, cost reduction, and overall strategic advantage. Here’s How:

- Strategic Value Creation: By aligning procurement activities with organizational goals and objectives, procurement transformation enables the procurement function to contribute strategically to the overall success of the business. Through enhanced supplier collaboration and innovation, organizations can leverage digital procurement transformation to build stronger relationships with suppliers, drive product and service innovation, and make informed choices that optimize resources and enable them to capitalize on opportunities.

- Improved Procurement Efficiency: Procurement transformation streamlines and optimizes procurement processes, reducing manual tasks, eliminating bottlenecks and accelerating cycle times. Automation of manual tasks and workflows enhances efficiency by freeing up valuable resources, reducing errors and minimizing administrative overhead. Improved efficiency enables organizations to bring products and services to market faster and respond more quickly to customer demands.

- Cost Reduction: Procurement transformation optimizes spend management by identifying cost-saving opportunities, negotiating favorable terms with suppliers and eliminating wasteful spending. Economies of scale and standardized procurement processes help to reduce costs and increase purchasing power, contributing directly to the bottom line and enhancing financial performance.

- Enhanced Transparency: Procurement transformation increases visibility into procurement activities, providing stakeholders with real-time access to data and insights. This helps to ensure compliance with regulations and policies, and reduce the risk of fraud and corruption. Transparent procurement processes build trust and confidence among customers, investor and regulatory agencies, as well, strengthening the organization’s reputation and brand integrity.

- Quality Enhancement: Procurement transformation focuses on ensuring product and service quality standards through rigorous supplier evaluation, monitoring and management. Robust quality assurance processes and performance metrics enable organizations to identify and address quality issues proactively, reducing the risk of defects and recalls, ultimately improving customer satisfaction.

There has also been a rapid rise of procurement technology adoption in recent years, and it has reshaped the landscape of modern supply chain management. The global procurement software market is projected to grow at a CAGR of 10.9% between 2022 and 2029, reaching $13.80 billion.

This surge in adoption is fueled by the need for organizations to navigate complex supply chains, optimize sourcing strategies and mitigate risks in an increasingly globalized and competitive marketplace.

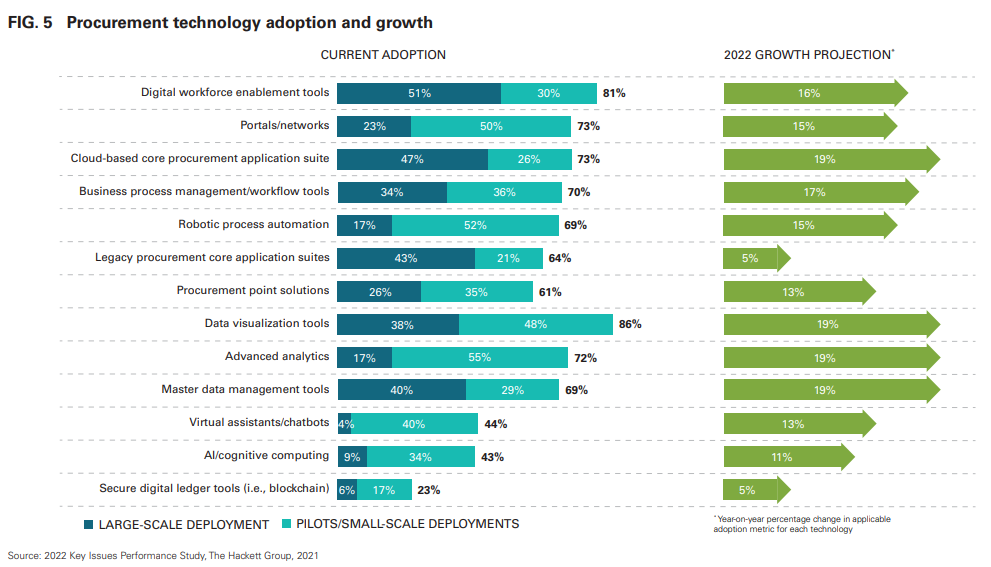

The figure below shows a breakdown from the 2022 Procurement Insights & Key Issues report by the Hackett Group, of the types of procurement technologies in which companies are investing.

Technologies such as those listed in the graphic above play a pivotal role in driving digital procurement transformation by revolutionizing traditional procurement practices and presenting various opportunities for organizations to enhance procurement efficiency, effectiveness and value creation.

- Advanced technologies such as artificial intelligence (AI), machine learning, robotic process automation (RPA) and blockchain automate manual tasks, providing real-time insights and enabling smarter decision-making.

- Cloud-based procurement platforms provide organizations with scalable and agile procurement solutions to streamline procurement processes, improve collaboration with suppliers and enhance visibility across the supply chain.

- Mobile procurement applications empower stakeholders to access procurement information and perform tasks on-the-go, further enhancing productivity and efficiency.

Pro Tip

Learn more about procurement transformation in our blog “Enabling Digital Procurement Transformation with The Hackett Group”.

Procurement Transformation: Creating Value For Your Organization

Procurement transformation now takes center stage for growing businesses everywhere. Organizational leaders see the value of supporting this critical strategic sourcing business endeavor ensuring all essential supplies are available when needed, and at the price and quality expected.

Optimize & Improve Processes

By analyzing existing processes, procurement professionals can identify areas for improvement, such as standardizing procedures, automating manual tasks, and implementing cost-saving measures.

Through continuous procurement process improvement initiatives, procurement can enhance efficiency, reduce cycle times, and lower operational costs, ultimately driving greater productivity and performance across the organization.

Achieve Compliance

Procurement helps achieve higher compliance by ensuring adherence to internal policies, regulatory requirements, and industry standards. By establishing robust procurement policies and procedures, conducting regular audits, and monitoring supplier performance, procurement can mitigate risks associated with non-compliance, such as legal penalties, reputational damage and supply chain disruptions.

Improve Visibility

Procurement facilitates transparency and accountability in procurement activities, providing stakeholders with real-time visibility into procurement processes, spending, and supplier relationships.

Through centralized procurement systems and reporting tools, organizations can track procurement activities, monitor spending trends, and identify potential compliance issues, enabling proactive risk management and decision-making. At its core, fostering robust supplier relationships stands paramount, coupled with the simplification of dialogue and transactional procedures.

By harnessing innovative vendor management tactics—including strategic supplier segmentation, meticulous performance assessments, and the integration of cutting-edge collaboration platforms—procurement serves as a conduit for a superior supplier experience. This paves the way for enduring partnerships, rooted in a foundation of trust and joint advantage.

Additionally, electronic procurement platforms and self-service portals enable suppliers to submit bids, manage contracts, and track payments efficiently, reducing administrative burdens and enhancing supplier satisfaction.

7 Steps For Creating a Successful Procurement Transformation Strategy

When devising a strategy for procurement transformation, it’s critical to consider your long-term goals and how you will create a future-ready procurement organization. Here are seven critical steps to take toward successful transformation:

- Assess current processes: Evaluate existing procurement workflows and practices to identify strengths and weaknesses. Audit your current tech stack for gaps or duplicate/overlapping capabilities and determine where data silos exist.

- Identify improvement areas: Pinpoint specific aspects of procurement operations that can be optimized, streamlined or automated to enhance efficiency and effectiveness.

- Develop a transformation roadmap: Create a strategic plan outlining goals, objectives, timelines and resources needed for executing your digital procurement transformation initiatives.

- Gain executive buy-in: Secure support and commitment from senior leadership by communicating the benefits and strategic importance of procurement transformation.

- Select and implement the right technologies: Identify and deploy appropriate technology solutions, such as procurement software and analytics platforms, to enable procurement process improvements and achieve desired outcomes.

- Continuous improvement and measurement: Establish metrics, key performance indicators (KPIs) and benchmarks to monitor progress, track performance and identify opportunities for further procurement optimization.

- Manage change: Proactively address resistance to change, provide training and support, and foster a culture of innovation and continuous improvement to ensure successful adoption of new processes and technologies.

Leveraging AI in Procurement Transformation

As we’ve learned, Generative AI in procurement plays a significant role in procurement digital transformation, offering innovative ways to enhance efficiency, reduce costs and improve decision-making processes. Its influence is evident across various parts of procurement transformation.

Generative AI can automate many aspects of the sourcing process, from generating Requests for Proposal (RFPs) to evaluating bids based on predefined criteria. It can also help teams create contracts by generating drafts based on learned negotiation strategies and organizational requirements. AI can analyze contracts for compliance and risk, as well, and generate alerts for renewals or renegotiations.

By automating content creation, Generative AI helps to minimize the need for creating content manually, saving time and effort for procurement professionals. AI can also take over repetitive, time-consuming tasks such as order processing, invoice matching and payment processing, freeing up human resources for more value-added activities.

Generative AI algorithms can analyze vast sets of procurement data to identify purchasing patterns, forecast demand and anticipate supply chain disruptions. It can also be used to optimize just-in-time inventory by predicting restock needs and executing purchases automatically, thereby reducing holding costs. By predicting supply chain disruptions, AI enables pre-emptive action to avoid stock-outs or production delays, enabling continuous operations.

Gen AI can alsoautomate time-intensive daily tasks such as: research, analysis, content creation, modification, and summarization. of a suppliers’ performance, reliability and risk levels as they sift through a variety of data – delivery times, quality ratings and compliance scores, for example.

With these insights, procurement teams can build stronger, more collaborative relationships with key suppliers and optimize their supplier base. And that’s not all – AI systems can continuously scan the market for evolving trends, new suppliers or alternative materials and products, becoming a source of competitive sourcing intelligence.

By leveraging AI in procurement, organizations are not just automating tasks, but are also creating a proactive, intelligent procurement environment. This drives down costs, enhances strategic insight and ultimately contributes to fostering innovation and a competitive edge in the marketplace.

Pro Tip

Learn more in our blog “Transforming Procurement with Generative AI”.

Future Trends in Procurement Transformation

Beyond transforming procurement processes, organizations must rethink how they measure success. As Natacha Tréhan, Professor in Purchasing Management at the University of Grenoble-Alpes, pointed out in a recent webinar, current procurement performance metrics are increasingly insufficient in a world facing polycrisis, regulatory changes, and resource scarcity.

Rethinking Procurement Performance

To adapt, companies need to integrate new performance measures into their systems:

- A real-time, dynamic risk management system is essential.

- Measuring resilience: Organizations should develop capacities to absorb, adapt, and transform in response to crises, using KPIs like business continuity scores and recovery times.

- Balance traditional profit-focused metrics with non-financial reporting, supported by advanced technologies.

Accelerating digitalization and leveraging AI as well as close collaboration with your value chain ecosystem on procurement performance will help organizations navigate the complexities of the modern business landscape more effectively.

Watch the full webinar: Transforming Procurement Performance from a Tactical Toolset to a Strategic Process.

Learn More About Why We Urgently Need A Paradigm Shift In Procurement Performance

Case Study: Piramal’s Procurement Transformation Journey

Piramal is a global leader in end-to-end glass bottle manufacturing providing packaging for pharmaceutical, perfume and specialty food and beverage industry. Piramal’s procurement organization was looking to gain visibility into spend, especially maverick spending, to improve forecasting.

They also wanted to improve their control over suppliers by managing all contract processes from a single place – from negotiation to signature and renewal. However they were held back by manual processes and legacy systems that made it difficult to collaborate with suppliers.

After implementing Ivalua’s Procurement Platform, the company gained transparency across all spend and the entire Source-to-Pay process. Results included:

- 19% annual cost savings over four years

- 75% reduction in process cycle time for contracts and catalogs

- 40% reduction in PR/PO cycle

“Ivalua’s Source-to-Pay suite was one of the best things we’ve done. Ivalua helped make things more efficient and brought so much transparency and value to Piramal.” – Samit Datta Head of Global Supply Chain & IT PIRAMAL

Watch this interview with Samitto learn more.

Launch Your Procurement Transformation With Ivalua

At Ivalua, we’ve embraced this digital procurement trend by empowering customers to swiftly initiate their transformation journey in a targeted way and progressively scale up to encompass broader spending and supplier needs. Our goal is to understand your transformation objectives and work with you to devise a tailored plan. With Ivalua’s procurement platform you can:

- Achieve Quick Wins: Through its comprehensive procurement platform, Ivalua enables quick wins with rapid supplier enablement. Not only does the platform streamline processes and enhance supplier collaboration, it allows organizations to start small and expand gradually, ensuring a smooth transition and rapid time to value.

- Expand to All Spend & Suppliers: With Ivalua, organizations can consolidate their procurement processes and data across all categories of spend and suppliers, providing a 360-degree, unified view of their procurement operations. The platform’s robust capabilities, including advanced procurement analytics, supplier management tools and procurement automation features, enable organizations to efficiently manage a diverse supplier base and optimize sourcing strategies.

- Unlock Your Competitive Advantage: By leveraging Ivalua’s technology and expertise, organizations can unlock new opportunities for innovation, cost savings, and growth, positioning themselves as leaders in their industry.

Let’s start taking stps to start your Procurement Transformation journey. Watch a demo of Ivalua’s Source-to-Pay platform in action.

Pro Tip

Download the Gartner® Magic Quadrant for Source-to-Pay Suites Report.

Conclusion: Redefining Modern Procurement Transformation

Venturing into the realm of procurement transformation is not just an undertaking; it’s a strategic leap towards securing a flourishing future in the rapidly changing business arena. By revolutionizing procurement operations, companies are poised to uncover a treasure trove of innovation, heightened efficiency, and unparalleled strategic value. It’s clear that as enterprises recalibrate and forge ahead, the modernization of procurement will be an indispensable catalyst in carving their path to triumph and establishing a competitive edge that will resonate through the emerging business epoch.

Modern procurement isn’t just about tightening the bolts; it’s about re-engineering the entire machine for peak performance in the global marketplace. The transformation isn’t simply a trend—it’s a business imperative that promises to redefine the essence of operational success.

Let's Get Started With Your Transformation With Ivalua’s Market-Leading Procurement Platform!

FAQs about Procurement Transformation

Procurement transformation helps organizations evolve from tactical purchasing to a strategic function that drives cost savings, risk mitigation, and business value. It improves efficiency, strengthens supplier collaboration, and aligns procurement with broader organizational goals.

Growing cost pressures, supply chain disruptions, regulatory demands, and rising expectations for sustainability and transparency are all driving transformation in procurement organizations. Companies are looking to modernize procurement processes and adopt more agile, data-driven strategies.

Digital procurement enables automation, standardization, and real-time visibility across the procurement lifecycle. With better visibility, teams can make smarter decisions, reduce cycle times, and improve compliance with policies and regulations.

Common challenges include resistance to change, lack of digital skills, and difficulties integrating new technologies with legacy systems. Data silos and inconsistent processes can also hinder transformation efforts.

AI, machine learning, robotic process automation (RPA), and cloud-based platforms are key enablers of transformation, providing support or smarter sourcing, risk management, analytics, and supplier collaboration at scale.

Further Reading

- Analyst Report: Procurement 2023: BIG Trends & Predictions

- 2022 Procurement Insights & Key Issues Results from The Hackett Group’s Annual Key Issues Study

- 2025 Gartner® Magic Quadrant™ for Source-to-Pay Suites

- Successfully Launching a Digital Procurement Transformation

- What is Procurement Transformation?